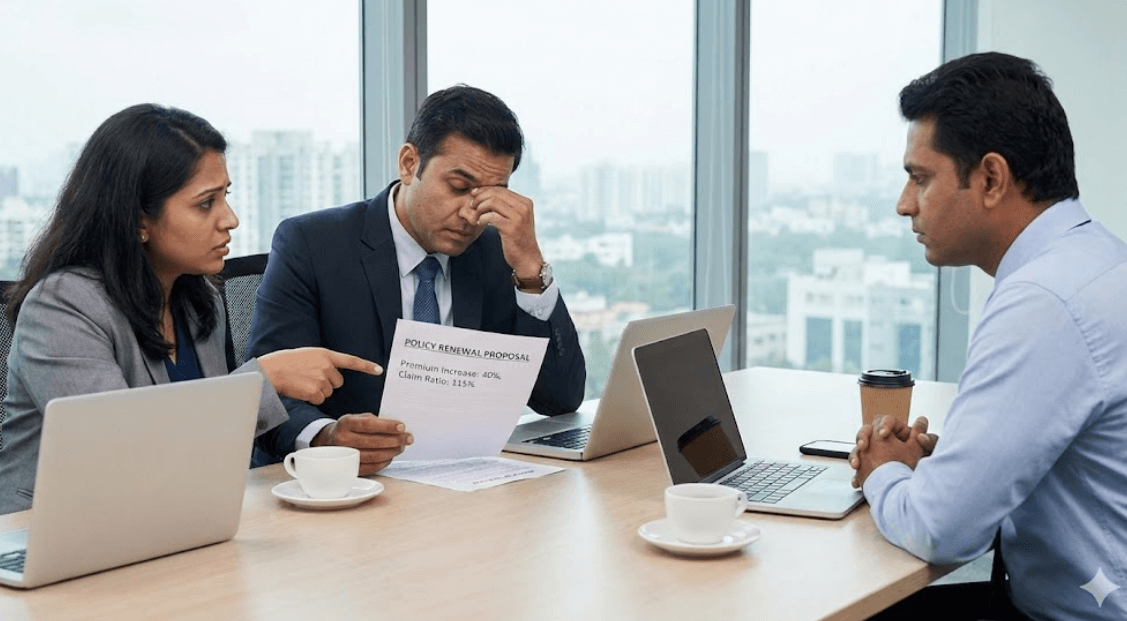

In India, the line between personal wealth and business liability is often blurred. Most entrepreneurs and traders rely on heavy credit lines—Overdrafts (OD), Cash Credit (CC) limits, and Term Loans—to fuel their operations.

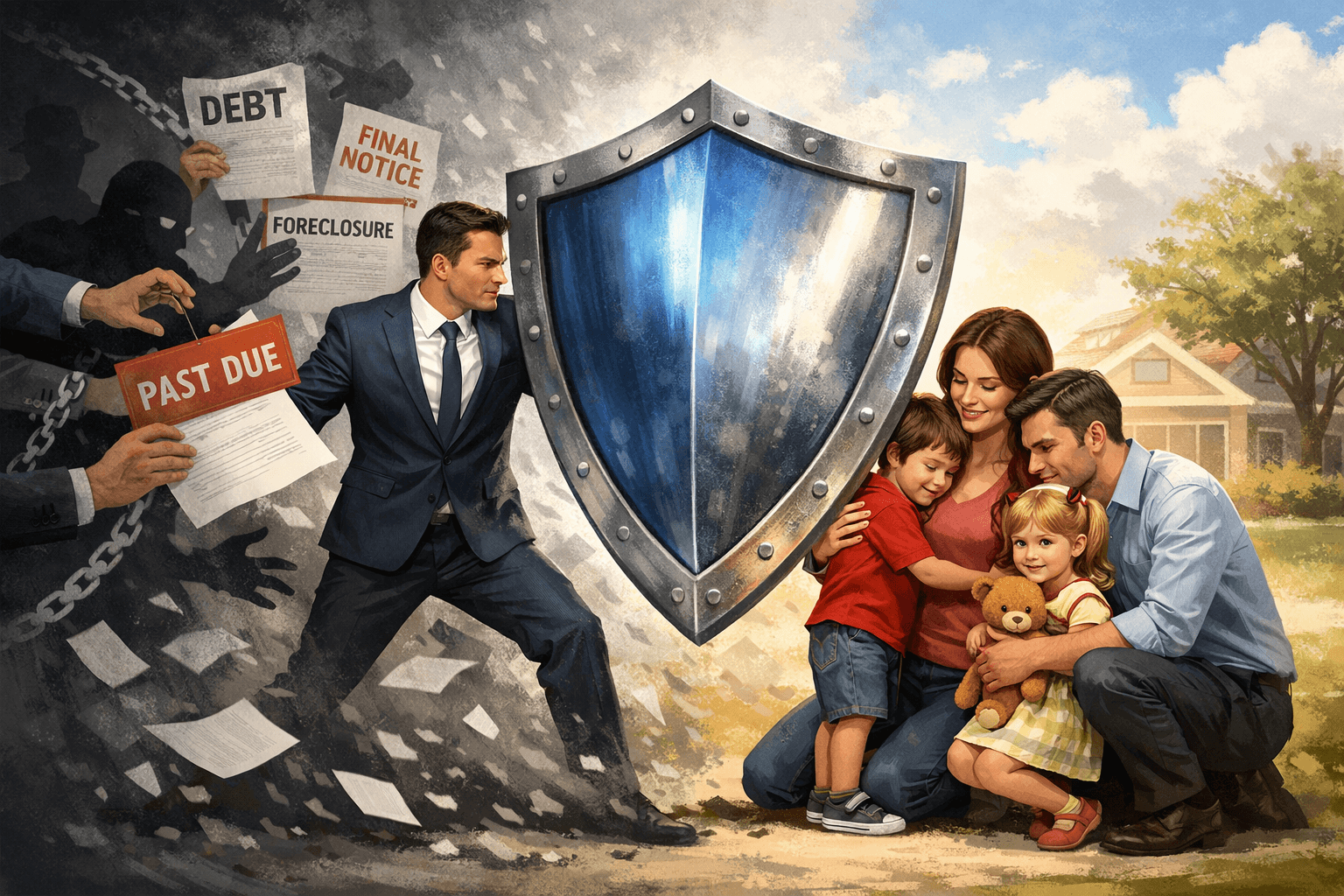

The hidden danger lies in the law: In the event of the business owner’s death, creditors have the first right over their estate. This includes real estate, bank balances, and crucially, standard life insurance proceeds. It is a tragic irony that the Term Insurance bought to protect the family is often seized by banks to settle business dues, leaving the widow and children with nothing but a paid-off company.

Mr. Gupta, a second-generation steel trader in Punjab, was running a high-turnover business. To expand operations, he had accumulated business debts of approximately ₹4.5 Crores across various banks.

Being a responsible family man, he decided to purchase a ₹5 Crore Term Insurance Policy to secure his wife and two daughters. He approached Disha Insurance simply to get the “lowest premium quote.”

During our financial fact-finding, we noted his significant business liabilities. We realized that a standard policy was dangerous; if he passed away, the banks would legally attach this ₹5 Crore payout to settle the ₹4.5 Crore debt.

We advised Mr. Gupta to purchase the policy under the Married Women’s Property (MWP) Act, 1874.

Mr. Gupta was initially reluctant about the extra paperwork but trusted our expertise and signed the addendum.

Three years later, tragedy struck. Mr. Gupta suffered a massive cardiac arrest and passed away. As is often the case, the business creditors arrived almost immediately. The banks moved to freeze his accounts and laid claim to his assets, including the life insurance policy, to recover the outstanding loans.

The creditors sent legal notices to the insurance company, demanding the payout be routed to them.

However, because Disha Insurance had structured the policy under the MWP Act, the insurer legally rejected the banks’ claims. The law was clear: the money did not belong to Mr. Gupta’s estate; it belonged to the Trust created for his wife.

Had Mr. Gupta bought the policy online or through an untrained agent, his family would have received only the leftover balance (approx. ₹50 Lakhs) after debt settlement. Because of our specific legal advice, they received the full corpus, allowing them to secure their future independent of the business’s fate. At Disha Insurance, we ensure your safety net actually holds when you fall.

Discover our comprehensive insurance services designed to protect, empower,

and simplify coverage for businesses and individuals.

Explore related case studies showcasing real results, proven strategies, and success stories to inspire smarter business decisions and growth.